Liquidity pressure worry as companies face worsening payment behaviour

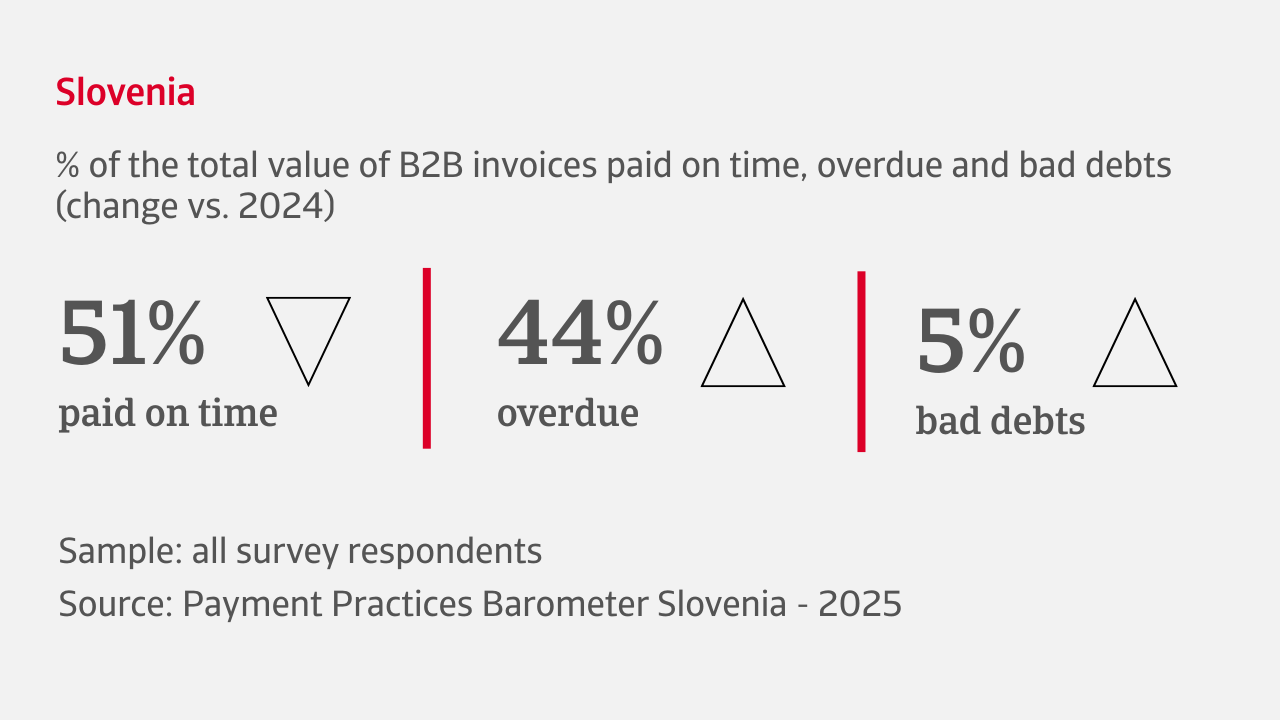

Our survey reveals increasingly challenging payment conditions in Slovenia, with most companies reporting a noticeable deterioration in the payment behaviour of B2B customers during recent months. A shift toward longer payment cycles is becoming more frequent, with overdue invoices now accounting for an average 44% of all B2B sales. The most cited cause is customer liquidity issues. Bad debts average 5% of all B2B invoices, a financial strain which is particularly acute in the automotive industry.

.2025-09-25-13-25-42.png)

45% of all B2B sales are currently transacted on credit among companies in Slovenia. While many sectors prefer upfront payments to safeguard cash flow, the automotive sector leans towards a more lenient trade credit policy, probably due to the need to stay competitive in a price-sensitive market and maintain order volume. Although payment terms largely remain unchanged, the average across industries now stands at around 50 days, with more firms reporting extensions than reductions.

Looking ahead

Insolvency surge fears prompt focus on working capital management

A mood of caution is clearly evident among businesses in Slovenia as they look to the year ahead. Two-thirds of companies anticipate a rise in business insolvencies during the coming months, raising concern around working capital management and overall liquidity health. Days Sales Outstanding (DSO) is expected to worsen by many companies as longer payment cycles become more common, potentially constraining cash flow further. While inventory turnover is projected to remain broadly stable, some firms anticipate liquidity being tied up in stock build-ups – working capital that could otherwise support daily operations.

Supplier payment timings (Days Payable Outstanding – DPO) are largely expected to remain unchanged, underscoring the key role that supplier credit continues to play in Slovenia as a buffer in tight liquidity environments. Despite these concerns, companies express cautious optimism about sales performance. Many expect revenues to hold up, even as profitability remains under pressure due to persistent cost challenges, particularly those linked to production input factors.

Slovenian businesses are preparing for a significant surge in insolvencies. Cash flow is tightening due to longer payment cycles. Against this backdrop, strategic customer payment risk management is essential, not optional

Industry insights

Pharma

More than half of pharma companies have recently expanded trade credit offerings to support B2B customers, but an average 41% of sales transacted on credit shows the industry still has a cautious approach to credit risk. Payment terms are mostly unchanged, at an average 51 days from invoicing, although a slowdown in B2B payments has been widely observed. Overdue invoices now affect 38% of B2B transactions, primarily due to customer liquidity shortages, a common issue in this capital-intensive sector. Bad debts currently average 3%, relatively modest, but still impactful in terms of cash flow and liquidity management.

Steel and metals

Cautious credit practices and growing concerns over liquidity are evident in this sector. An average 40% of B2B sales are conducted on credit, and most firms report stable payment terms, averaging 53 days from invoicing. While many companies observe no significant shifts in B2B payment behaviour, some say there is a slowdown in customer payments. Overdue invoices currently affect 45% of B2B sales, primarily due to liquidity constraints. These delays are particularly impactful given the sector’s capital-intensive nature and sensitivity to cyclical demand. Bad debts average 4% of B2B invoices, marking a notable increase that threatens cash flow and heightens liquidity pressures.

Automotive

The automotive sector is increasingly turning to trade credit to sustain business relationships and support B2B sales. Two-thirds of companies have increased trade credit offerings, with 54% of sales now made on credit. Most firms report unchanged payment terms, but a significant number have adopted more relaxed terms, which average 43 days from invoicing. Overdue invoices now affecting an average 49% of all B2B sales on credit. Liquidity constraints are the main reason in an industry where high input costs and long production cycles strain financial flexibility. Bad debts average 7% of B2B invoices, placing pressure on cash flow and liquidity.

Interested in finding out more?

For a complete overview of the 2025 survey results for Slovenia, download the full report available in the related documents section below.

To explore more on how these insights can strengthen your own credit risk strategy, speak with us at Atradius to see how we can help you stay ahead.

.svg "_Atradius Collections_C_Pos")