Login

Construction Industry Trends Belgium - 2023

Energetic renovation keeps up activity

.svg "_Atradius Collections_C_Pos")

Collections

Collections

Australia

Australia

Austria

Austria

Belgium

Belgium

Brazil

Brazil

Canada

Canada

China

Collections

China

Collections

Czechia

Czechia

Denmark

Denmark

Finland

Finland

France

France

Germany

Germany

Hong Kong

Hong Kong

Hungary

Hungary

India

India

Indonesia

Indonesia

Ireland

Ireland

Italy

Italy

Mexico

Mexico

Netherlands

Netherlands

Poland

Poland

Portugal

Portugal

Singapore

Singapore

Spain

Spain

Sweden

Sweden

Switzerland

Switzerland

United Kingdom

United Kingdom

United States

United States

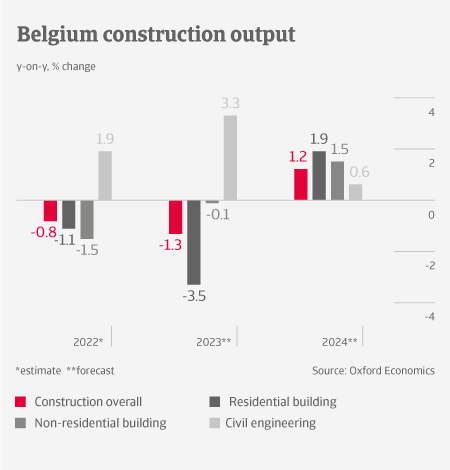

In 2023, we expect Belgian construction output to contract 1.3% after a 0.8% decrease in 2022, mainly due to lower activity in the residential and industrial construction segments. Both suffer from high inflation and increased financing costs for building activities. Only civil engineering output is expected to grow this year (by about 3%), supported by public investment in clean energy and infrastructure projects. The renovation work segment focused on energetic renovation (heating, ventilation, isolation and renewable energy) remains resilient, because it benefits from government support (VAT decrease).

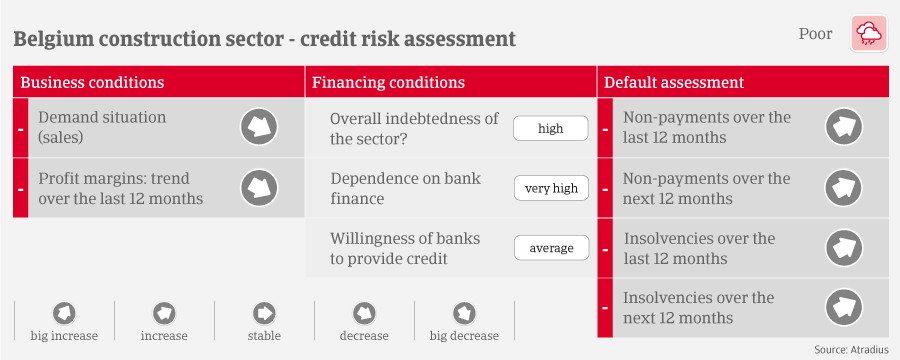

Many businesses are highly indebted, and a combination of high prices for energy, building materials and increased wage expenses is putting high pressure on margins. Belgian construction companies operate in a very competitive environment, in particular in the public tendering business. Passing on higher input costs is very difficult, because prices have usually been fixed for a longer period of time.

According to the latest Atradius Payment Practices Barometer, Days Sales Outstanding (DSO) in the Belgian construction industry averaged more than 60 days during the past 12 months. This clearly points to the issue of late payments and consequent pressure on business cash flow. As an immediate measure to avoid liquidity shortage, businesses are delaying payments to their own suppliers, with the resulting danger of a domino effect through the industry supply chain.

Due to the sluggish economic performance outlook for this year, rising high input prices and the expiry of (pandemic-related) government support measures we expect that both payment delays and insolvencies will increase further in 2023, with construction business failures expected to rise by more than 20% this year.

We assess the credit risk situation as “Poor” for the residential and non-residential subsectors and as “Fair” for civil engineering and construction materials. Even though demand should pick up again in 2024 and inflationary pressures abate, skilled labour shortage will remain a serious challenge. There is a lack across all levels, from engineers to calculators, site managers, yard supervisors, to all types of construction and installation workers. This will have a negative impact on the completion of construction projects and will increase wage costs for builders in the future.