Login

Turkey battles high inflation ahead of elections

Regardless of the election result, the next Turkish government faces a complicated set of macroeconomic problems

.svg "_Atradius Collections_C_Pos")

Collections

Collections

Australia

Australia

Austria

Austria

Belgium

Belgium

Bosnia and Herzegovina

Bosnia and Herzegovina

Brazil

Brazil

Bulgaria

Bulgaria

Canada

Canada

China

Collections

China

Collections

Croatia

Croatia

Czechia

Czechia

Denmark

Denmark

Finland

Finland

France

France

Germany

Germany

Hong Kong

Hong Kong

Hungary

Hungary

India

India

Indonesia

Indonesia

Ireland

Ireland

Italy

Italy

Mexico

Mexico

Netherlands

Netherlands

North Macedonia

North Macedonia

Poland

Poland

Portugal

Portugal

Romania

Romania

Serbia

Serbia

Singapore

Singapore

Slovenia

Slovenia

Spain

Spain

Sweden

Sweden

Switzerland

Switzerland

United Kingdom

United Kingdom

United States

United States

With general elections approaching, the Turkish economy is struggling with high inflation, a weak lira and the impact of the earthquakes that took place in February. The upcoming general elections for the presidency and parliament on May 14 are set to be a particularly close contest, potentially resulting in divisive court challenges, which could unleash political instability.

President Erdogan’s Justice and Development Party (AKP) is polling around 34% of the vote, as of May 8 according to PolitPro. The runner-up Republican People’s party (CHP) is polling just below 30% of the vote. Polls indicate the opposition bloc (“Nation Alliance”), consisting of six parties, is close to gaining a majority, but nothing is certain yet. The presidential election is likely to be a close race between Erdogan and the main opposition candidate, Kemal Kilicdaroglu (CHP). While Kilicdaroglu has a slight edge over Erdogan – 49% vs. 43% respectively – the chances that he will surpass the 50% threshold required to declare victory is still tight. This would require a run-off presidential vote on May 28.

The incumbent Justice and Development Party (AKP) came to power more than two decades ago with the promise of structural reforms to address a series of economic and financial crises since the late 1990s. Their structural reform programme laid the foundation for more sustainable growth by taming rampant inflation. It also significantly reduced the public debt ratio and putting the banking sector on much more solid footing. Turkey enjoyed a period of solid GDP growth between 2009 and 2018, fuelled by cheap foreign borrowing and characterised by robust domestic credit growth. The credit bubble eventually burst as the lira sold off in 2018 and a more modest growth trajectory followed. Nevertheless, the economy was quite resilient during the coronapandemic. Turkey was one of the few G20 countries that managed to avoid a recession in 2020 and showed a solid growth recovery in 2021 (11.4%).

Growth declined to 5.6% in 2022 and we expect it to slow further to 1.0% in 2023, barring any major changes to the direction of economic policy. Economic activity is constrained by high inflation and a weak lira that are weighing on consumer purchasing power. Furthermore, slowing export growth and the negative impact of the earthquakes (which are assessed by Oxford Economics to be in the order of 0.3 to 0.4 percentage points) are also weighing on GDP growth. An expansionary fiscal policy does provide some counterweight to growth slowdown, but it is likely that the government will cut down on spending after the elections are over. We expect period of slower growth over the next 10 years as less abundant global liquidity and slower credit growth keep economic activity on a more modest trajectory. Current macroeconomic imbalances are likely to remain prominent in the coming years, potentially leading to volatile growth.

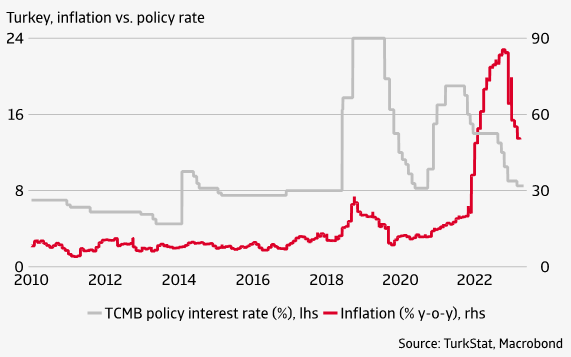

One of the key vulnerabilities of Turkey’s economy is high inflation, caused by an ultra-loose monetary policy, credit-driven growth and high global commodity prices. Since September 2021, the key central bank policy rate was reduced by 10.5 percentage points to 8.5% in March this year, despite very high inflation. The inflation rate rose to 85% year-on-year in October and November 2022 (figure 1). Despite easing somewhat in recent months due to favourable base effects, inflation remains very high (in April 2023 it was 44% y-o-y).

We expect the central bank to continue its unorthodox policy at least until the elections. After the vote, however, a major tightening of the policy rate seems unavoidable to stabilise the lira. The lira has been a major casualty of the central bank’s policy stance. Since the easing cycle started, it has depreciated by 34% against the USD. The central bank attempts to manage pressure on the lira through capital controls and interventions on foreign exchange markets. But the ability of the central bank to intervene in the currency market is constrained by the limited amount of FX reserves. Therefore, the main instruments to combat lira weakness are capital controls and other macroprudential measures. Exchange-rate protected deposit account (known as KKM) are used. These offer depositors protection against a depreciation of the lira against major currencies such as the USD and the EUR. Other measures target banks and businesses that hold large FX deposits or earn mostly in foreign currencies. For instance, an export-oriented company operating in Turkey must convert up to 40% of their foreign currency export receipts into Turkish lira. These measures, however, did not prevent a further depreciation of the lira since early 2023. We expect the lira to gradually depreciate further against other major currencies in 2023-2024, given political uncertainty and external imbalances.

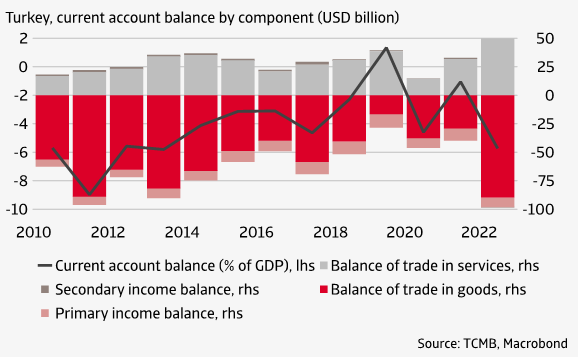

Another vulnerability of Turkey’s economy is its weak external position, characterised by structural current account deficits and high external debt. The current account deficit widened to 5.7% of GDP in 2022 (figure), and we forecast that it remains wide in 2023 at 4.5%. The main factor driving the wide current account deficit is the rising import bill, specifically of energy imports. As energy and raw materials are denominated in USD, the weakness of the lira only has a limited positive effect on the current account. We forecast the current account deficit to narrow in 2023-2024 as slowing economic growth curbs the rise in imports, while lira depreciation boosts exports.

Turkey has large external financing needs, including short-term external debt repayments and current account financing. We estimate that the gross external financing need was USD 245 billion in 2022, or about 30% of GDP. We forecast that the external financing requirement will increase in 2023-2024 to an average of USD 267 billion. Foreign-exchange reserves currently cover less than 30% of the external financing requirement. To meet its financing requirement, Turkey relies heavily on short-term borrowing, making it vulnerable to a balance-of-payments crisis in the coming years.

Government finances remain sound, despite higher spending. We expect the government deficit to widen in the near term, from 0.9% of GDP in 2022 to 4.2% in 2023 , due to social-spending initiatives ahead of the elections, including high public wages and pension increases, early retirement (potentially benefitting up to 2.1 million employees) and debt forgiveness for certain utilities and student loan payments. In addition, the earthquake relief and reconstruction will also add pressure to fiscal accounts. The government has already allocated TRY 100 billion (USD 4.8 billion) to relief efforts, and directed transfers to affected families, unemployment compensation and announced the postponement of tax payments in the region. Meanwhile, revenue is likely to slow as the economy weakens. In the medium term, the fiscal deficit is likely to decrease as the government is expected to rein in spending after the elections.

We estimate the government debt to have been 32% of GDP in 2022. Public debt is likely to increase to 36% in 2023. A vulnerability of the fiscal position is that an increasing percentage of public debt is denominated in FX (more than 70% in 2023, up from around 40% in 2017). However, fiscal sustainability risks in Turkey remain relatively low. The government maintains a comfortable position with low public debt as a share of GDP and historically low deficits and thus has some scope for stimulus in another economic downturn.

The banking sector as a whole is well capitalised, with a Tier 1 capital ratio of over 16.8% and a capital-adequacy ratio of 19.5% in Q4 2022. The non-performing loan (NPL) ratio stood at 1.9% in February 2023, but this partly reflects a more lenient classification regime: from early 2020 the Turkish authorities classified a loan in the worst NPL category only when it was 180 days overdue, rather than 90 days previously. High inflation and monetary easing have sent short-term real interest rates into negative territory, risking a disruption in credit intermediation. The banking sector is exposed to Turkey's heavily indebted private sector, which has already been experiencing difficulties in rolling over its debt, one-third of which is denominated in foreign currency. The risks to Turkey’s banking sector are clearly increasing, vulnerable to the lira’s developments. Given the sector’s still-healthy metrics and track record of resilience through economic and financial crises, our baseline view is that this will be maintained this year.

To conclude, the winners of the upcoming Turkish elections will be inheriting a highly vulnerable economy, grappling with soaring inflation, a structural account deficit and a high dependence on short-term foreign capital inflows. With global monetary policy tightening and domestic policy space tightening, the urgency to return to more conventional policy to get inflation under control and reduce Turkey’s external imbalances is rising. Some change to policy under the next government is seemingly inevitable, but election promises do not reflect this.

The incumbent AKP is committed to alleviating this situation post-elections by maintaining accommodative monetary and fiscal stances while relying on unconventional macro-prudential policies to ensure liquidity. In the case that Erdogan would reverse the direction of his economic policy by shifting to interest rate hikes, past policy u-turns and uncertainty will keep investors wary. In case the opposition succeeds, following through on their promises to return to policy orthodoxy – including inflation-targeting monetary policy and improving central bank independence – will be easier said than done. The cohesiveness of the opposition, comprised of six parties from across the political spectrum, still needs to be tested.

Whether the AKP or opposition wins this May, we can be confident that the political situation will remain highly polarised, keeping policy uncertainty elevated and increasing the risk of instability. The extent of economic challenges and depth of external vulnerabilities ensure that any pivot to more conventional policies will be a difficult and gradual process. Hiking interest rates would be the first step towards preventing capital outflows and rebuilding FX reserves but would also spur the first annual contraction in economic activity since 2009.

Theo Smid, Senior Economist

theo.smid@atradius.com

+31 20 553 2169

Dana Bodnar, Economist

dana.bodnar@atradius.com

+31 20 553 3165

All content on this page is subject to our Disclaimer, available here.